So you’re looking at your monthly payments, a car loan, a student loan and a bunch of credit cards. And you’re wondering how do I get out from under all this debt? How do I lower my monthly payments? You’ve heard of this thing called a debt consolidation loan, and your wondering, is debt consolidation a good idea?

For some debt consolidation can be an effective way of lowering the interest rate on their debt. And by doing so lower their monthly payment. However, from my own experience, I think the benefits are often overstated. If you’re considering a debt consolidation loan consider these three things first.

What is Debt Consolidation?

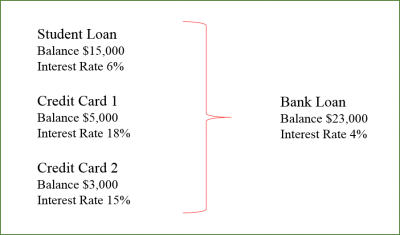

Debt consolidation is when you take out a loan to consolidate other forms of debt. For example, you take out a loan from your local bank to pay off credit cards, a student loan, or vehicle loans.

Debt consolidation is a means of reducing the number of “debt” accounts you have so you have a single loan payment. And generally a lower interest rate. The idea is that if you can consolidate all your payments into a single payment and a lower interest rate you will be able to pay your debt off faster. Debt consolidation can take place in a couple of different ways.

- A loan from your local bank in the form of a personal loan or a home equity loan. Personal loans are loans generally provided in two to five-year terms with a fixed monthly payment. Personal loans are unsecured, meaning they are not backed by any collateral. A home equity loan is where you borrow against the equity in your home (secured loan) to finance the consolidation of your debt. Personal loans because they are unsecured often come with a higher interest rate. Large banks like Wells Fargo and Bank of America also provide consolidation loans.

- Credit card balance transfer offers. These types of loans are offered by credit card companies. The companies allow you to transfer balances from other accounts to a credit card. They then provide a grace period, generally 12-21 months where no interest is charged. The perspective is that by transferring interest earning accounts to a non-interest bearing credit card, you will be able to pay off your debt faster. Discover, Capital One and Citi are just some of the credit card companies providing balance transfer offers.

Debt consolidation is also viewed as a means of improving your credit score.

However, is debt consolidation right for you? Here is a different perspective on debt consolidation. One that is less about monthly payments and interest rates and more about how you got into debt in the first place.

Related Posts:

- How to Pay Off Debt Using the Snowball Method

- Understanding The Debt Trap From the Outside In – The Marketing of Debt in America

- How Many Credit Cards Should You Have? My Credit Score with One Credit Card

- 10 Successful Money Management Tips to Live By – from a 52-Year-Old

- How Surviving Wisconsin Winters is Like Managing Your Money

- How to Make a Car Last Forever, How to Save $30,000 in a Lifetime

My Story and Debt Consolidation

Many years ago when I graduated from college and received my first “real” job, I made the determination, because of my new income level that it was acceptable to have three credit cards. Most of this was due to the fact that I was making more money than I had ever made before. And all that money gave me a sense of confidence – that I could pay for anything, including my credit card debt.

About a year after using those credit cards I found myself with some pretty high credit card balances. I knew I probably needed to do something to get them paid off.

Enter debt consolidation.

I used a 0% balance transfer offer through one of those credit card companies (you know the ones that advertise on TV and all over the Internet) to consolidate all my debt onto one credit card. I had a year to pay off the new credit card with no interest so I figured I was in pretty good shape and on track to eliminating my debt.

Fast forward one year later. How many credit cards did I have? 4

The credit card I had transferred my other balances to never got paid off. In addition, the other three credit cards I had now had new balances. For me, debt consolidation only made my situation worse.

You’re probably thinking that debt consolidation would have worked for me if I had a little more self-discipline.

Of course, you’re right, but at the time I was young had a new job and as far as income goes the sky was the limit. I believed that more money would eventually fix my credit card problem.

What You Need to Know – A Perspective on Debt Consolidation

I eventually dug my way out of debt and if you’re in debt you can too. But before you head down the debt consolidation road, here are three things to consider.

- The only ones that really promote debt consolidation as a debt pay off strategy are those companies that provide credit – banks, credit unions, and credit card companies offering personal loans or a 0% balance transfers. That’s because they are in the business of making money by loaning you money so you can pay them for your debt. They understand that if you’re struggling with debt it’s unlikely you will pay off your loan early or make more than the minimum payment on the loan.

- Debt consolidation provides a false sense of accomplishment. If you currently receive five different statements every month, and you now only receive one, that can feel pretty good. Like your debt consolidation loan fixed all your problems, but did it? Think about it, all you really did was move your debt from five different accounts to one. Even if your interest rate is lower, you still have to pay off the balance. Debt consolidation often provides a false sense of relief and by doing so removes the sense of urgency needed to effectively manage your debt.

- This is the big one. Using credit and accumulating debt to make purchases is emotional and behavioral. It’s not about interest rates or a single loan payment and it’s definitely not about debt consolidation. If you believe it’s acceptable to use credit to make purchases then regardless of how often you consolidate your debt, you will end up back in debt. Change how you think about the use of credit is the only way to manage your way out of debt.

Is Debt Consolidation a Good Idea?

There are situations where debt consolidation loans make sense. Especially when a significantly lower interest rate on large balances can lower your monthly payment and save you a bunch of money. However, before you make the assumption that debt consolidation is a good idea, be sure you ask yourself how you got into debt in the first place.

Disregard all the advertising mumbo jumbo you hear in the media about debt consolidation. Forget the fact that a single statement and lower monthly payment will make you feel good. And start by challenging your beliefs about why you’re spending and why you need to use credit in the first place.

For me, once I made the decision not to use credit as a means of purchasing items I was able to work my way out of debt in no time. Not pursuing debt consolidation options forced me to look at why I was using credit in the first place. Changing my beliefs and then my behaviors are what got me out of debt.

Is debt consolidation a good idea? From my experience NO. Debt consolidation loans just make you feel better about your situation and may actually prolong the time you stay in debt.

Helpful Resources:

- Credit Karma – Free Credit Score, Monitoring & Insights

- Filling The Pig – Workbook, create your own get out of debt plan.

- Credit Card Pay Off Calculator

What are your thoughts on debt consolidation? Comment below.

Sign up for a Kindle Unlimited 30 Day Free Trial and read the complete Filling The Pig finance series of books for free.

I spent a great deal of time to locate something similar to this

Glad you found it. Thanks Kevin

Wish I had found you last week – just did a balance transfer to consolidate debt – none were too large, just there if you can understand that feeling. Only good thing is, it was to a card I already had, and only had a transfer fee of 1%. Now I just need to pay it off in 8 months – and pry the cards from my hubby’s hands so he doesn’t use them again . . . any suggestions for that?

Lisa, thanks for writing. Have been down the debt consolidation path myself and understand the feeling. The first step to fixing any problem, including debt, is self-awareness – sounds like your already there. As far as your hubby goes. From my own past experience, I can tell you that having your spouse on board makes the whole debt payoff process a lot easier and faster. I would recommend both of you sitting down adding up all your credit card payments and then discussing what your future would look like if you didn’t have them. From the perspective of the opportunities that would be created without debt – your stress level, lifestyle, where you live and how you live. I can tell you that once I kicked my credit card debt it was one of the most liberating things I ever did. If you haven’t already you may want to check out this article on using only one credit card – it may help with the transition process How Many Credit Cards Should You Have? My Credit Score with One Credit Card

Thanks again for writing – stay focused, and stay the course you will get there.