The average car loan payment in the U.S. is $450/month. It may seem like an impossible feat, but if you want to stop making car payments you need to learn how to pay cash for a used car. Buying with cash and buying used is the only way to make sense of a car purchase.

Americans Love Their Cars

It goes without saying that most of us love our vehicles – cars, trucks, and minivans (OK, maybe not minivans). Not from the perspective that we are enthusiastic car collectors, but from the perspective that we value reliable transportation. For some, a car represents a dependable means of getting back and forth to work or maybe shuttling the kids to soccer practice. For others a car represents a boost for our egos, maybe it’s a “cool” car, or maybe it’s a sign of prestige – a sign we finally made it.

Regardless of where you sit on the vehicle buying spectrum we all understand that purchasing a vehicle is a major expense.

They Are Expensive!

For most, the ability to purchase a vehicle requires taking out a loan. To some degree, this is understandable considering the average cost of a new vehicle is about $30,000. We often justify the purchase of a new vehicle because in our minds there more reliable, they typically come with a warranty and they look and smell great.

The reality is that in our lifetime the purchase of a vehicle will be one of the worst investments we will ever make. Where else do you spend tens of thousands of dollars on an asset and over time have it continually depreciate (Lose value).

Don’t misunderstand me, a reliable, great looking vehicle is important to me as well. However, in the interest of staying out of debt and saving money, let’s take a different approach and perspective on purchasing a car – a viewpoint that does not include taking out a loan. A perspective that starts with paying cash for a used car. Which then allows us to stop making car payments.

Related Posts:

- How to Make a Car Last Forever, How to Save $30,000 in a Lifetime

- Budgeting Questions: Should You Spend on Your Car or Home

- Why I Buy Vehicles with Cash – I Just Spent $2,500 on Repairs and I’m Loving it

- The Art of Being a Cheapskate – How I Successfully Manage My Budget

- How I Made Over $30,000 in 4 Months Flipping Stuff – How to Flip Stuff and Make More Money

- 10 Successful Money Management Tips to Live By – from a 52-Year-Old

Let’s Start with Some Facts

If you currently have a vehicle loan or are contemplating taking out a loan to purchase a new car, truck or minivan, consider this.

- The average cost of a new car is $30,000. A new truck $40,000.

- The average American will purchase 6-7 vehicles over a lifetime. That means our lifetime investment will be anywhere from $180,000-$280,000.

- Depending on the type of vehicle you purchase, the average depreciation level will range from 15-25% per year over the first five years. That means your new vehicle loses value in the first five years something like this. Let’s assume you purchase a new vehicle for $30,000. And it depreciates 10% (which is conservative) each year in the first five years.

- Immediately after you drive your new car off the dealership lot, its value drops by 10% or $3000, your new car is now a used car valued at $27,000

- At the end of year one, the value drops another 10%, $2700. Your new car is now valued at $24,300

- Year two, another 10%, $2430, value $21,870. You get the point!

- By the time your car is five years old your car has depreciated by almost 50% and is now worth only $15,000.

Don’t Get Upside Down

- Get a new car, pay a new car premium. Obviously, rates vary based on driver age, coverage and deductible, but it’s not uncommon to pay over $1000 annually for car insurance. Because that new vehicle is being financed, you will need full coverage, which means a higher premium.

- Flexible financing options of 48, 60 and 84 (7 years) months means more drivers are able to purchase a new car because of the lower monthly payments. However, consider this. You finance the purchase of a new car for seven years, pay interest on the loan, which increases the total cost of the vehicle. Then, at the same time, the vehicle is depreciating – almost 50% over the course of the seven-year term. Depending on the type of vehicle you purchase and the depreciation, it’s possible by year seven your car is worth less than the value of the loan you used to finance it with. (this is often called upside down on a loan – you owe more on the loan then the value of the vehicle)

So What Does This All Mean?

It means paying cash for a used car is the only way to go. If you’re trying to save money, pay off debt, and trying to create a new lifestyle for yourself, taking out a car loan is…well, rather inconsistent.

Financing a new vehicle purchase has become almost a standard when it comes to purchasing vehicles. And not just new vehicles, but used ones as well. Too often we focus on the monthly payment of the vehicle, and what we can afford. And disregard the other critical aspects of the purchase – like depreciation, interest costs, and higher insurance premiums.

So what’s the solution to buying your next vehicle?

FTP recommended. Want to hone your used car buying skills, be sure to read Everyone’s Guide to Buying a Used Car and Car Maintenance, Scotty Kilmer

Pay Cash for a Used Car and Stop Making Car Payments

Does this sound like an insurmountable proposition? Like climbing Mt. Everest on a windy day. Well, if you’re used to making a vehicle payment then buying with cash can seem pretty unlikely. (Believing you have to finance a vehicle is a Self-limiting Belief, be sure to read my blog post Do You have Self-Limiting Beliefs about Money.)

However, let’s take a moment and consider the possibility of paying cash for a used car.

First, and foremost the only way to establish a “cash” car buying strategy is to be able to save money. As discussed in my eBook Filling The Pig there are enormous opportunities that start to present themselves once you start saving cash and eliminating debt. Buying a car with cash is one of those opportunities.

Second, you have to be able to think of purchasing a vehicle as an upgrade process. The first used vehicle you purchase with cash breaks the car loan debt cycle. Each subsequent purchase after that (because you’re saving more and more money) allows you to afford a better-used vehicle and improves the reliability of the vehicle you’re driving.

Keep these critical factors in mind when you think about paying cash for a used car.

- A used vehicle does not necessarily mean less reliability. Cars are manufactured much better these days, most will run for 175,000 miles or more without any major maintenance issue.

- When you’re buying used your insurance premiums will be less. And if you’re already saving money, you can increase the coverage deductible and further lower your premium. This means more money to save for your next used car upgrade.

- When you buy used you forego the most expensive depreciation years on a vehicle – typically the first five years. (you save even more money)

- Keep in perspective we are using this strategy to purchase vehicles over our lifetime – 6-7 vehicles, Not just a single onetime purchase.

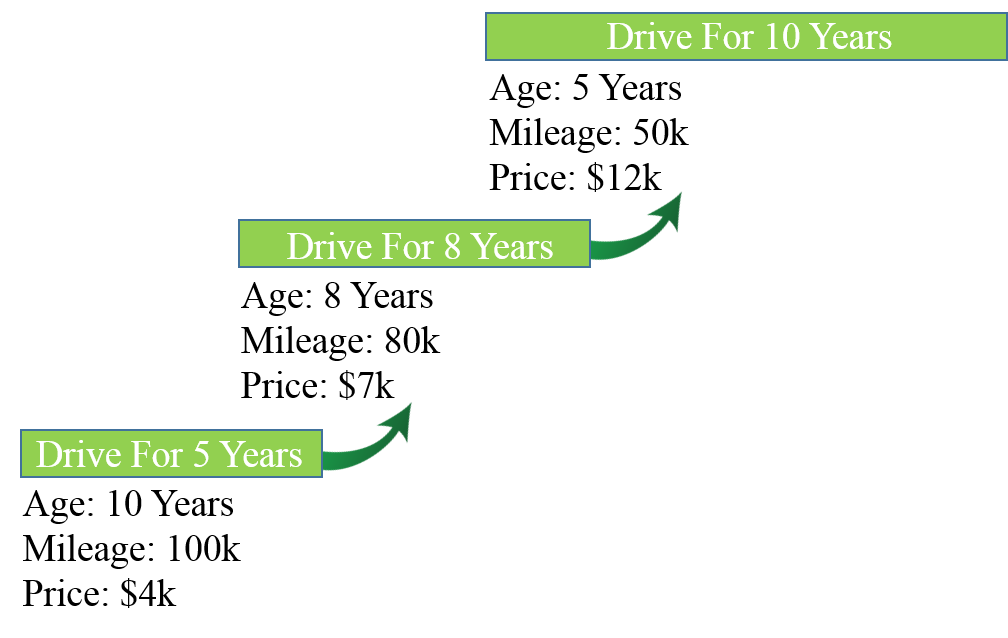

The illustration below starts in the lower left with the purchase of your initial used car, then progresses up and to the right with each vehicle upgrade.

- Age represents how old the used vehicle is when you purchase it.

- Mileage is the approximate number of miles on the vehicle when you purchase it, based on an average of 10,000 driving miles per year.

- Price is what you paid to purchase the vehicle – with cash.

- The green bars represent the number of years you own the vehicle before your next upgrade.

As you can see after the initial cash purchase, you’re upgrading to a better vehicle with each purchase. An earlier model with lower miles. Upgrading improves the reliability of the vehicle allowing you to drive it for a longer period of time. The longer you can drive the vehicle, the more time you have to save money to purchase that next upgrade. But most important is the money you are saving because you stopped making car payments.

For this vehicle buying strategy to work there are some additional points, you need to understand.

- The reliability of the used vehicle you purchase dictates the length of time you drive the vehicle without any major maintenance needs. New brakes, oil changes, tires are considered minor maintenance and applicable to even a new car. Major maintenance issues like a faulty transmission, or an engine that is about to fail are the most important things to consider. Before you purchase that used vehicle, ask a friend or someone you know, or maybe a mechanic to inspect the vehicle. Want to learn more about vehicle maintenance, be sure to read Auto Repair for Dummies, by Deanna Seclar

- Also, in relation to purchasing a reliable used vehicle. High miles do not necessarily represent a less reliable vehicle. A vehicle that has low miles but has not been taken care of can represent an even higher maintenance risk. High mileage vehicles like those from rental agencies or those with highway miles can represent an excellent opportunity for purchase. Typically, these types of vehicles will come with maintenance records which help confirm they have been well taken care of. Again, check with someone you know or a mechanic.

- Don’t back yourself into a corner and limit you’re used car buying options. You may want that Jeep Wrangler, Toyota Camry, or Honda Pilot. However, the more you narrow your options to a specific model the less likely you will find that next great deal on a used vehicle. Keep your options open, be patient and remember your goal is to upgrade to that next great vehicle you do want. It probably won’t happen with your first cash purchase but it will happen in time.

Finally

Not able to make that initial $4,000 used car purchase? This strategy works regardless of how much you can initially save for that first purchase. The age and reliability of the vehicle may limit the length of time you own it, but the strategy is the same. Save money to upgrade to something better.

Concerned about saving enough cash? Look at it this way. The average new car monthly loan payment in the U.S. is $450. Annually that represents a cost of $5,400. Over five years that’s $27,000. If you can stop making car payments, and stick that money in the bank. You can pay cash for a used car and eventually buy the car of your dreams.

Leveraging this cash buying strategy is another way of limiting your exposure to debt. If you had a vehicle loan payment in the past, saving money to make that first vehicle purchase can seem intimidating. But once you make that first cash purchase, you will never go back to making monthly payments on a vehicle. Stay focused, be patient and you will pay cash for a used car and stop making car payments.

Recommended Resources:

- Everyone’s Guide to Buying a Used Car and Car Maintenance, Scotty Kilmer

- Auto Repair for Dummies, by Deanna Seclar

- Make that used car shine try Nu Finish – The best once a year car wax I have ever used.

Do you pay cash for used cars? Comment below.

Sign up for a Kindle Unlimited 30 Day Free Trial and read the complete Filling The Pig finance series of books for free.