Actually, the real question might be – how many credit cards should you have based on what the credit card companies think? Here is how I manage my credit score of over 800 with one credit card.

Ever since I started blogging about personal finance topics I have wanted to write an article focused on credit cards. Specifically the number of credit cards you should have. Because I believe effective credit card management is important if you’re trying to manage debt, save money and create wealth. Before I started writing this article I did a quick search on Google. I wanted to see what others were saying in regards to how many credit cards you should have. Then balance those opinions with my own.

I wasn’t shocked at the number of articles that have been written recommending how many credit cards you should have. What did take me by surprise was the fact that most of them recommended having 3-5 credit cards to manage your personal finances. Some even as many as seven. In fact, the other aspect that popped out from my quick Google search is that there were actually articles written that focused on developing a credit card strategy. Strategies that focused on how to leverage credit cards to maximize your cash back offers, improve your credit score and buying power.

Yikes!

Do you think there is any correlation between the number of credit cards being recommended and the fact that the average credit card debt in the US is almost $16,000? Or maybe the fact that almost 69% of Americans have less than $1,000 in their savings account. (Forbes) When it comes to personal finance I have heard of debt pay off strategies, money-saving strategies, and investment strategies, but credit card strategies?

In the past, I had my share of credit card debt and that debt was typically associated with multiple credit cards. If you’re trying to get out of debt or just looking to re-home your money management skills, here is a different perspective on credit cards (from past experience), and the number of credit cards you should carry.

The Need for Multiple Credit Cards

In most cases, the justification for having multiple credit cards and the marketing of credit cards is based on these benefits.

- Improve your credit score – more credit cards allow you to establish credit and improve your credit score.

- Maximize your buying power – more cards increase your buying power because you have more credit to leverage.

- Earn points to get airline miles – earn free airline tickets for a vacation with your family.

- Save 10% on purchases when you shop at your favorite store. Save money on in-store purchases when you use your favorite retailer’s store card.

- Earn Cash Back – When you charge items on your credit card, the credit card company gives you cash back. This math never made sense to me. They give you 1% cash back and then charge you 20% interest when you don’t pay the credit card off at the end of each month. (i.e. this type of math will keep you in debt)

Of course, there is nothing wrong with any of these reasons other than the fact all of them are based on the fact you make purchases using your credit cards.

Related Posts:

- Why Debt Consolidation is a Bunch of Crap

- The Marketing of Debt in America.

- 2 Little White Lies We Tell Our-self to Justify Spending with Credit Cards

- 4 Tips to Pay Off Credit Card Debt Fast

- What You Shouldn’t Do with Your Holiday Credit Card Debt, and How to Avoid a Repeat Next Year

- The Most Important Credit Card Alert You Need to Know – Now!

- 10 Successful Money Management Tips to Live By – from a 52-Year-Old

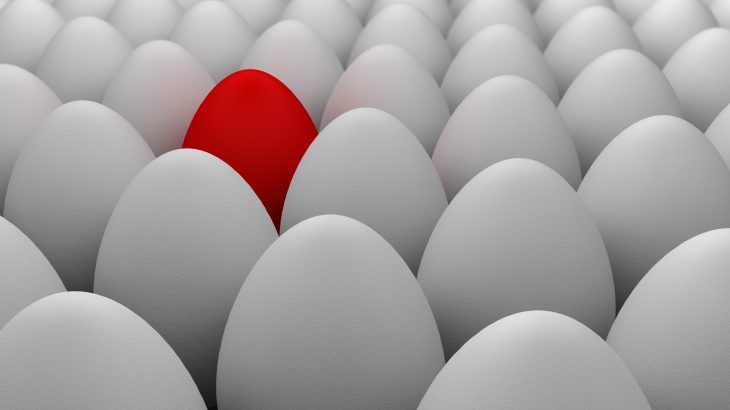

With Credit Cards, More is Never Better!

So How Many Credit Cards Should You Have?

Just One!

If you’re struggling with debt or just trying to do a better job of managing your money more credit cards for any reason won’t help. More cards actually create a distraction from focusing on what is really important, either getting out of debt or saving more money.

My past experience with credit cards has taught me this.

- Fewer credit cards mean fewer monthly statements to manage. If you have five credit cards and each card has a balance you’re “writing” five checks every month. One credit card = less clutter, fewer bills to pay, less stress.

- One credit card means you probably know what you’re balance is at all times. Multiple credit cards mean you’re probably not sure how much you have charged or what the balance is. The perfect environment for over-charging.

- Monitoring the activity on one credit card is far easier than monitoring three cards, especially when it comes to identifying credit card fraud.

- Your wallet will be thinner and take up less space. (This may or may not be important depending on who you are, I personally like it)

Many years ago when I tackled my own credit card debt, I got rid of all my credit cards but one. I have had the same personal credit card for over 25 years. And I don’t have this card because it has the lowest interest rate, provides cash back or because I accumulate bonus points. I have stayed with a single credit card because on three separate occasions I was a victim of credit card fraud. And in all three cases, the fraudulent charges were caught before I noticed them and it saved me a whole bunch of money.

How I Manage My Credit Score and Finances with One Credit Card?

There will no doubt be numerous opinions on the number of credit cards you should have. And arguments on how to use those cards. However, here is how I use my personal credit card to successfully manage my finances and maintain a credit score of over 800.

- My balance is paid off at the end of every month. I never carry a balance. You won’t become debt free or create wealth paying 20+% interest annually. While you earn 1% on the money in your savings account. No matter how you look at it the math doesn’t work.

- My credit card is a Capital One credit card. I don’t mess with Macy’s, Walmart, Best Buy or any retail store credit card. My perspective is that I want a credit card from a company that is in the credit card business. Not from a retailer who is providing a credit card to get me to spend more at their store. In addition, not having a credit card from a retailer assures I don’t get inundated with all their marketing material. (This isn’t a plug for Capital One. Only a recommendation that you get a credit card from one of the major credit card providers)

Monitor your credit score to avoid credit card fraud and improve security.

- I use my credit card for online purchases only. I never use my bank debit card because of my past experience with online fraud – I don’t want anyone messing with my checking or savings account. In addition, Capital One has proven to me that they can catch instances of fraud before I can so it provides me with a level of security.

- I do charge some utility bills like my cable to my credit card. Initially, I did this because I ordered the service online. I left it that way because it is convenient and I do earn bonus points for something I am going to pay every month anyway. (I.e. versus charging items on your card for the sole purpose of accumulating points.)

- I monitor my credit score through a free credit card monitoring company like Credit Karma. A single credit card coupled with a credit card monitoring service allows me to keep tabs on my credit score and any suspicious activity. (maybe I am being paranoid because of my past credit card fraud, but identity theft is on the rise and I just feel better about another means of monitoring my credit) You can sign-up for Credit Karma’s free credit monitoring services here.

If you’re concerned about your credit score because someday you want to buy a home, you could view having a single credit card as a detriment to obtaining a home loan. Especially if you believe the current buzz that more credit cards are better.

Or, you could look at it from this perspective.

In addition to your credit score, financial institutions when providing loans love it when you have money in your savings account.

If having a single credit card allows you to improve your credit score by successfully managing your credit. And it helps you simplify your finances and save more money. Then your credit card becomes less important to obtaining a loan for your new home.

(Years ago I flipped and rented real estate as a side business. I financed most of those homes through my local bank. The bank loved my credit score of over 800, but what they really liked was the fact I had a whole bunch of cash in my savings account. Having a single credit card never kept me from securing a real estate loan.)

Finally, effective credit card management isn’t just about the number of credit cards you have or your credit score. It’s about improving all aspects of your personal finance environment. Simple is better. Simplifying your environment with a single credit card allows you to focus on what’s important. Saving money, creating wealth and creating opportunities.

Helpful Resources:

- Read more Credit Card Wisdom articles here.

- Best Identity Theft Protection Services

- Top Selling Money Management Books at Amazon

- Credit Karma – Free Credit Score, Monitoring & Insights

Sign up for a KindleUnlimited Free 30 Day Trial and read the complete Filling The Pig finance series of books for free.

How many credit cards do you think you should have? Comment below.